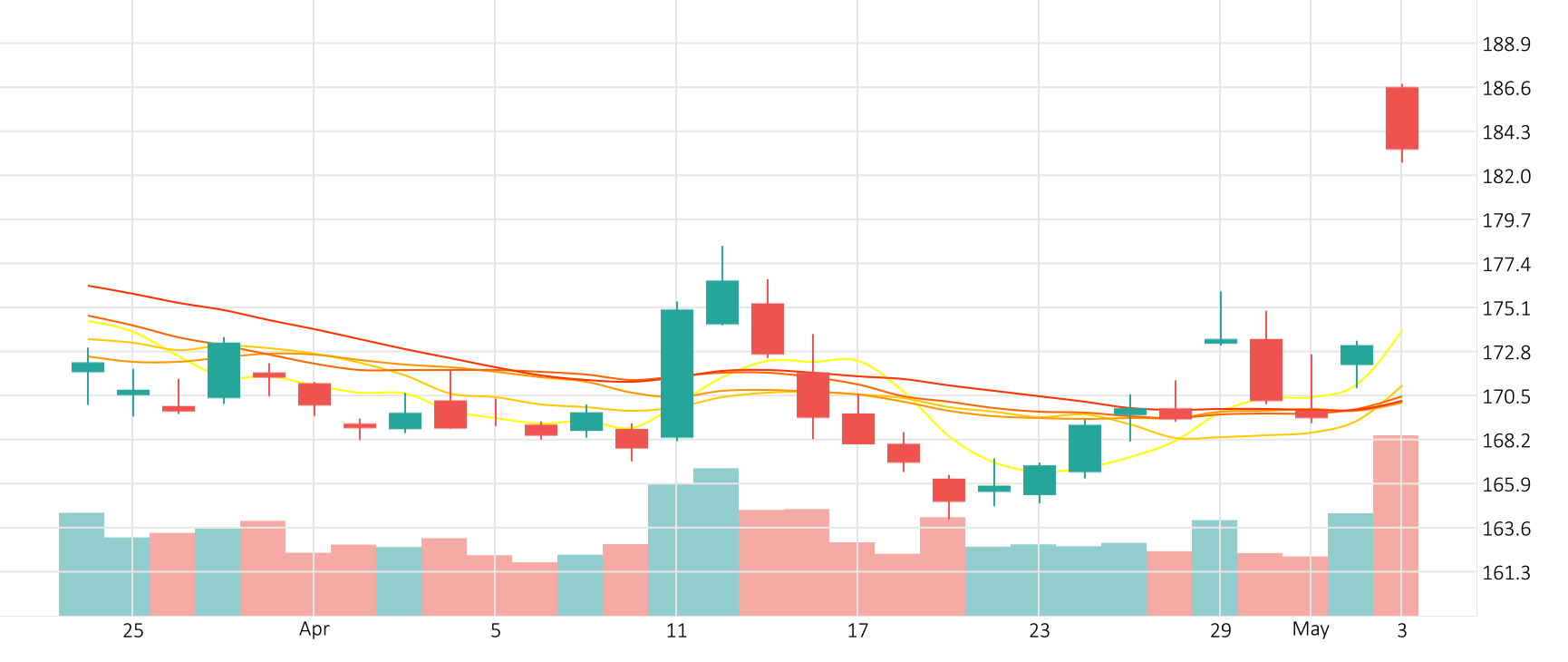

The “Magnificent Seven” stocks sank, extending a market rout that has wiped off around $2 trillion from their combined value as investors worry about the financial fallout of U.S. President Donald Trump’s global tariff war. Apple traded around 1-year low.

Shares of Apple crashed 6.3% in the last session. The Ultimate Oscillator is giving a negative signal.

Support: 171.29 | Resistance: 208.94