The U.S. dollar weakened against major currencies including the yen and euro, while China’s offshore yuan hit a record low, amid trade disputes sparked by President Donald Trump’s sweeping tariffs that have roiled markets for three days.

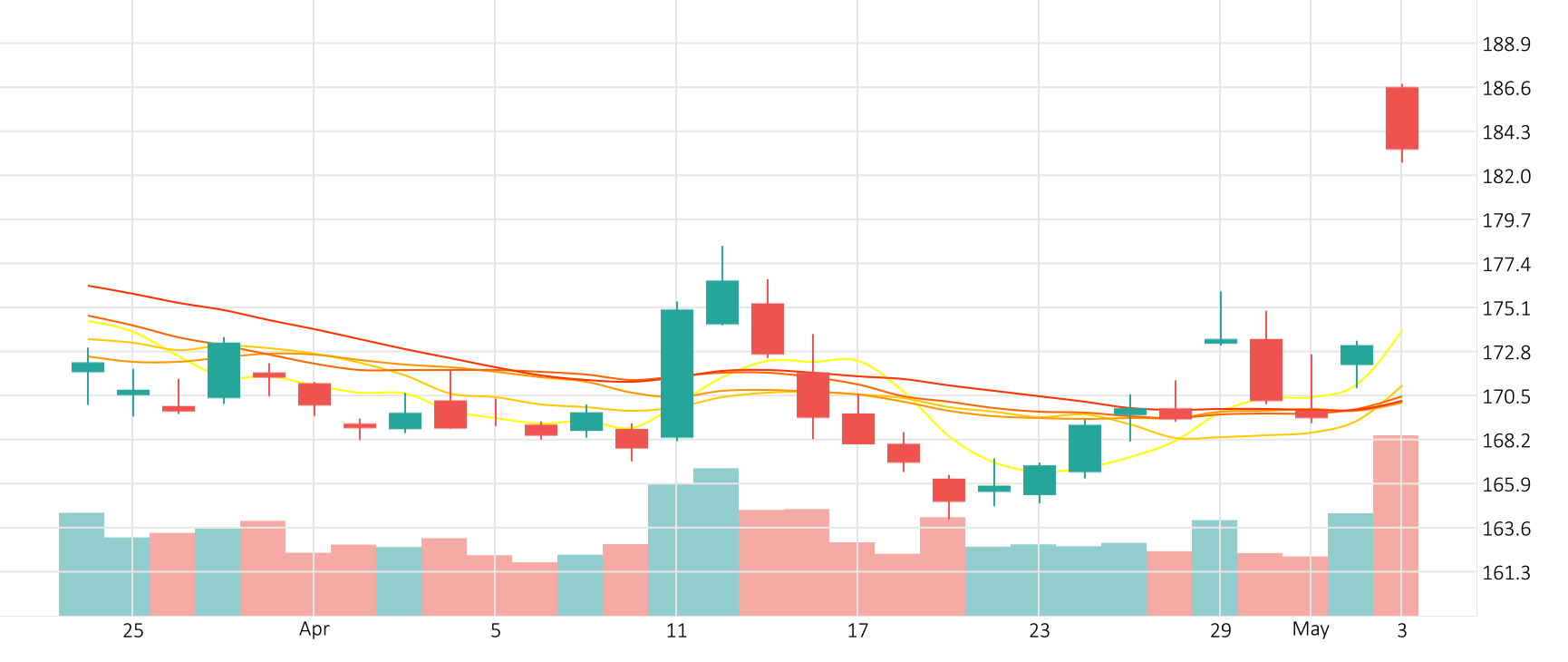

The Dollar-Yen pair fell 0.9% in the last session after gaining as much as 1.0% during the session. The CCI is giving a positive signal.

Support: 143.48 | Resistance: 149.48