The dollar stabilised, edging up from a three-year low against the euro as risk sentiment improved, but also held near a six-month trough against the yen as investors worried about the impact of U.S. President Donald Trump’s trade tariffs on the U.S. economy.

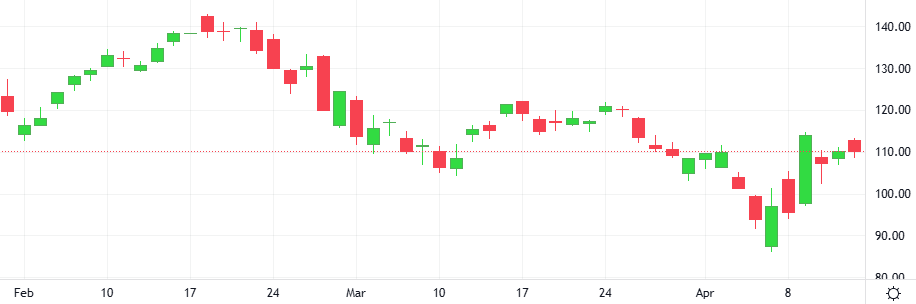

The Euro-Dollar pair fell 0.4% in the last session. The ROC is giving a positive signal.

Support: 1.1125 | Resistance: 1.1466