European shares were on course to post their worst week in three months on Friday, as U.S. President-elect Donald Trump’s comments about potential tariffs on the European Union further spooked investors already worried about the rate outlook.

European shares were on course to post their worst week in three months on Friday, as U.S. President-elect Donald Trump’s comments about potential tariffs on the European Union further spooked investors already worried about the rate outlook.

U.S. consumer spending increased in November amid strong demand for a range of goods and services, underscoring the economy’s resilience, which saw the Federal Reserve this week projecting fewer interest rate cuts in 2025 than it had in September.

Oil prices settled higher after U.S. crude inventories fell and the U.S. Federal Reserve cut interest rates as expected, but gains were capped as the Fed signalled it would slow the pace of cuts.

The Oil-Dollar pair rose 0.8% in the last session. The Stochastic indicator is giving a positive signal.

Support: 68.43 | Resistance: 71.91

Cryptocurrency exchanges in Europe are continuing to support Tether’s USDt stablecoin, even after Coinbase announced its delisting for European customers to comply with upcoming regulatory requirements. Top exchanges, including Binance, Crypto.com and Kraken, have retained trading support for Tether’s USDt.

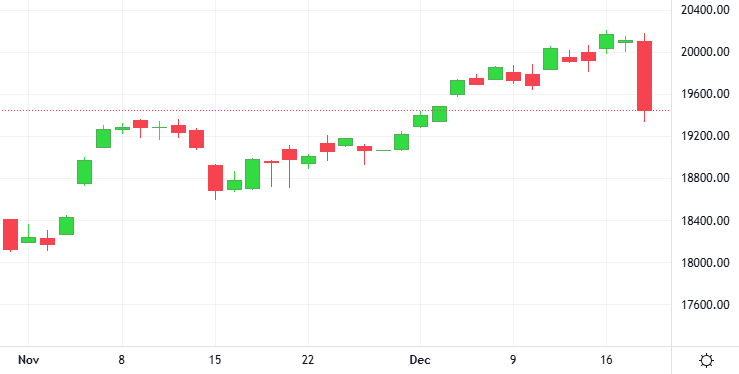

After a 2.7% dip during the last session, the Bitcoin-Dollar pair closed with a 1.2% drop. The Williams indicator is giving a negative signal.

Support: 99546 | Resistance: 109236

U.S. stocks fell, erasing earlier gains after the Federal Reserve cut interest rates by a quarter of a percentage point and the central bank’s economic projections signaled a slower pace of cuts next year. The Fed cut rates by 25 basis points to the 4.25%-4.50% range.

The U.S. Federal Reserve cut interest rates and signaled it will slow the pace at which borrowing costs fall any further, given a relatively stable unemployment rate and little recent improvement in inflation. U.S. central bankers now project they will make just two quarter-percentage-point rate reductions by the end of 2025.

Gold slipped under pressure from a strengthening U.S. dollar and climbing Treasury yields as investors focused on the Federal Reserve’s final policy meeting of the year with growing expectations of a gradual pace of rate cuts in 2025.

The Gold dipped a slight 0.2% against the Dollar in the last session. The RSI is giving a negative signal.

Support: 2608.8 | Resistance: 2685.3