Cryptocurrency exchange-traded funds accounted for 13 of the 25 largest ETF launches in 2024 by year-to-date inflows, according to a post on the X platform by Nate Geraci, president of The ETF Store, an investment adviser specializing in ETFs.

Cryptocurrency exchange-traded funds accounted for 13 of the 25 largest ETF launches in 2024 by year-to-date inflows, according to a post on the X platform by Nate Geraci, president of The ETF Store, an investment adviser specializing in ETFs.

The dollar edged down but remained within striking distance of its highest level in almost two weeks as investors’ focus moved to a U.S. jobs report due at the end of this week. U.S. payrolls will be crucial after Federal Reserve chair Jerome Powell pivoted from a battle against inflation to a readiness to guard against job losses.

Shares of Amazon exploded 3.3% in the last session. According to the Stochastic-RSI, we are in an overbought market.

Amazon’s stock skyrocketed 3.3% in the last session.

The Stochastic-RSI points to an overbought market.

Support: 168.9267 | Resistance: 175.8867

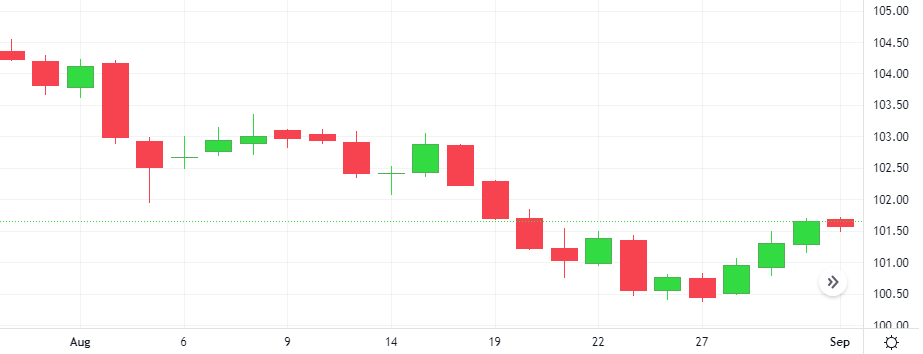

Oil prices retreated on Friday as investors weighed expectations of a rise in OPEC+ supply starting in October, alongside dwindling hopes of a hefty U.S. interest rate cut next month, following data showing strong consumer spending.

The Oil-Dollar pair fell 2.5% in the last session after gaining as much as 1.1% during the session. According to the CCI, we are in an oversold market.

WTI/USD dove 2.5% in the last session.

The CCI points to an oversold market.

Support: 72.271 | Resistance: 77.691

The Canadian dollar held on to much of its monthly gain against its U.S. counterpart on Friday as investors expect the global economy would avoid recession and Canadian GDP data did little to alter expectations for Bank of Canada interest rate cuts.

Bitcoin holdings of publicly listed companies have increased by almost 200% in a year, from $7.2 billion to $20 billion. Bitbo data shows that 42 publicly listed companies hold 335,249 Bitcoin worth roughly $20 billion.

The last session saw the Bitcoin drop 0.3% against the Dollar. The CCI is giving a negative signal.

Support: 55252.6667 | Resistance: 65464.6667