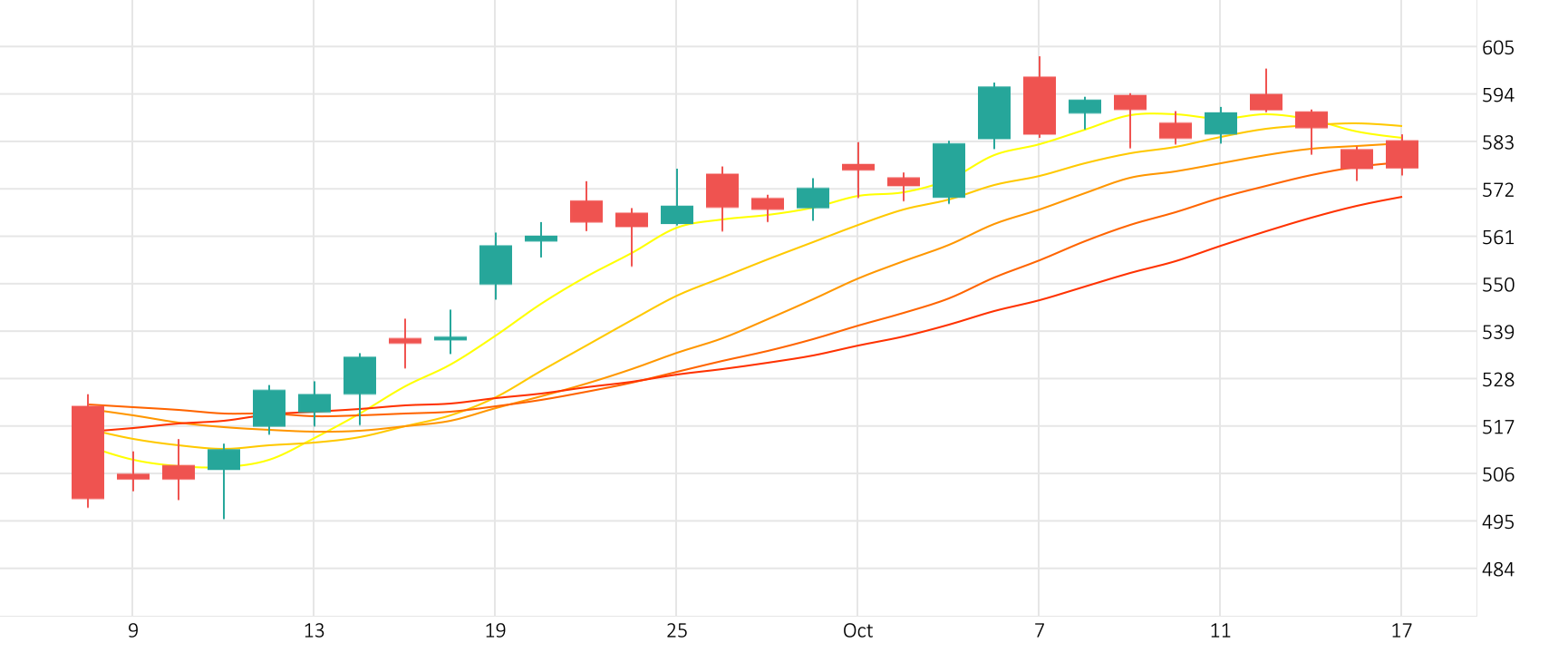

The price of Bitcoin reached $100,000 for the first time in history, marking a milestone for the cryptocurrency market after a year of significant growth. Bitcoin hit the $100,000, breaking a psychological level just weeks after reaching the $90,000 milestone on November 12th.

The Bitcoin saw a slight dip against the Dollar in the last session. The Ultimate Oscillator is giving a positive signal.

Support: 92613 | Resistance: 99705