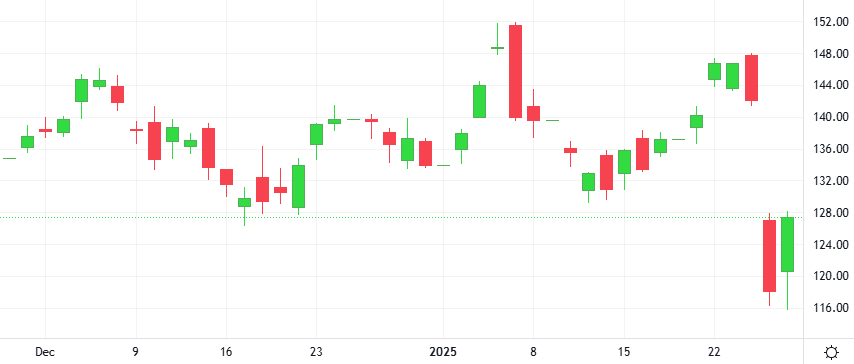

Short sellers of artificial intelligence-related stocks raked in bumper profits after the smashing debut of low-cost AI models from China’s DeepSeek spooked Wall Street, with bets against Nvidia yielding record profits totaling more than $6 billion.

Short sellers of artificial intelligence-related stocks raked in bumper profits after the smashing debut of low-cost AI models from China’s DeepSeek spooked Wall Street, with bets against Nvidia yielding record profits totaling more than $6 billion.

Siemens Energy, the world’s biggest maker of offshore wind turbines, reported on Monday a preliminary first-quarter revenue of $9.4 billion, up 18.4% on a comparable basis and slightly above consensus estimates.

Business intelligence firm MicroStrategy has proposed a stock offering to raise cash for “general corporate purposes,” including acquiring more Bitcoin, signaling its intent to continue accumulating the digital asset. MicroStrategy intends to offer 2.5 million units of its perpetual strike preferred stock.

The S&P 500 and the Nasdaq dropped, as the surging popularity of a low-cost Chinese artificial intelligence model knocked shares of chipmaker Nvidia and other companies benefiting from investments into the technology. Chinese startup DeepSeek has rolled out a free assistant it says uses cheaper chips and less data.

The Federal Reserve’s first meeting of 2025 in the coming week stands to test the resurgence in U.S. stocks as investors gauge the extent of more equity-friendly interest rate cuts in the months ahead. Stocks swooned after the Fed’s last meeting in December, when the central bank downgraded its forecast for rate cuts.

Oil prices settled slightly higher on Friday but posted a weekly decline, ending four straight weeks of gains, after U.S. President Donald Trump announced sweeping plans to boost domestic production while demanding that OPEC move to lower crude prices.

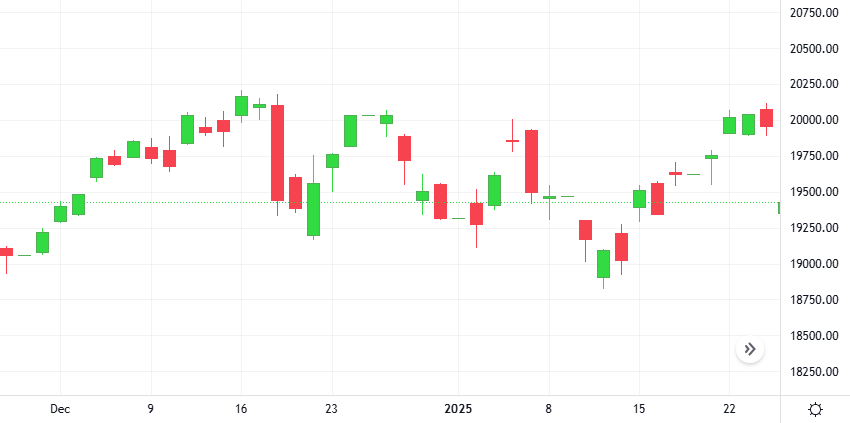

The Oil-Dollar pair gained 0.4% in the last session. According to the CCI, we are in an oversold market.

Support: 72.65 | Resistance: 76.16