Asian markets were modestly higher on Friday for the most part following a strong overnight rally on Wall Street that was sparked by the market beating earnings report from Nvidia. Investor sentiment is remaining somewhat subdued in Asia though as investors continue to worry over the health of the Chinese economy and the ongoing geopolitical disruptions in Israel and the Ukraine.

In Japan the Nikkei was unchanged as investors took a break for the Emperor’s Birthday holiday, just one day after Japan’s benchmark index roared to a new all-time high.

In Australia the S&P/ASX 200 climbed 0.4% higher to lead gains for the region, helped by solid gains from the big four banks. Shares of ANZ added 1%, NAB advanced by 1.1%, Commonwealth Bank was 0.3% higher, and Westpac also posted a 0.3% gain. The major miners saw more modest gains, with BHP rising by 0.6% and Rio Tinto ending flat with a slight gain of less than 0.1%.

Mainland Chinese markets extended their rally into a ninth consecutive session, despite the ongoing concerns over the health of the Chinese property market. The benchmark Shanghai Composite finished 0.6% higher, while the smaller cap Shenzhen Composite added 0.3%. Over in Hong Kong the Hang Seng underperformed, slipping lower by 0.1% on the day.

In South Korea the Kospi edged up by 0.1%, and in Taiwan the Taiex advanced by 0.2%.

Southeast Asian markets were mixed as Malaysia’s KLCI rose by 0.2%, but Singapore’s Straits Times Index retreated by 1.2% to lead losses for the region.

The S&P-500 is into a great positions today after marking another peak value as investors looked to end the week on a high note.

The Dow Jones Industrial Average gained 114 points, or 0.3%. The Nasdaq Composite advanced 0.1%.

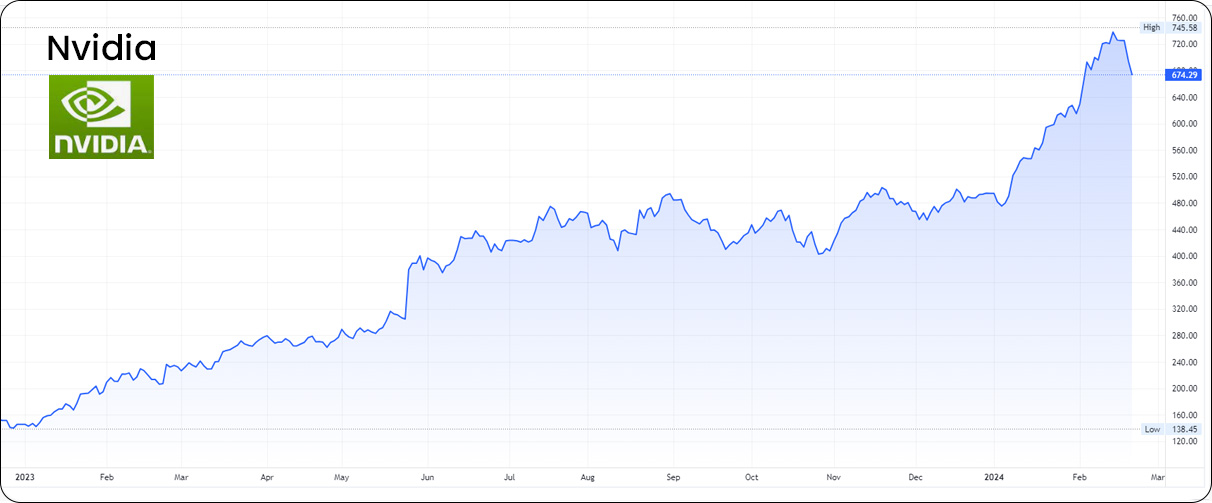

Wall Street is coming off a monster session as Nvidia shares roared higher on strong quarterly results, leading the chipmaker to surpass a $2 trillion valuation.

The United States today imposed new package of sanctions against Russia, targeting more than 500 people and entities. This is marking the second anniversary of Moscow’s invasion of Ukraine.

President Joe Biden announced that the new measures target to ensure Russian President Vladimir Putin ” pays even a higher price for military actions.

Block shares rallied more than 14% after the company announced surprise quarterly earnings and issued strong full-year guidance for gross profits.

Investors have been anxiously awaiting the latest quarterly results from Nvidia, and on Wednesday after U.S. markets closed they got what they’ve been waiting for. And they weren’t disappointed.

The technology company, which has been at the forefront of the hype over AI, reported sales and earnings that beat expectations from the Street, and also forecast better than expected results in the current quarter. The company reported earnings per share of $5.16 adjusted versus $4.64 expected on revenue of $22.1 billion versus $20.62 billion expected.

Nvidia management also forecast $24 billion in sales for the first quarter of 2024, while analysts have been expecting a more modest $22.17 billion.

Nvidia has been one of the prime beneficiaries of the ongoing AI boom, thanks to its cutting edge processors that are being used to train and run the massive large-language models that run AI tools like Chat-GPT.

Nvidia CEO Jensen Huang also assuaged investor fears that growth will soon slow for Nvidia. He said that demand will remain strong through 2025 and beyond thanks to the growth of generative AI throughout much of the business world.

Nvidia’s revenue was up 265% from the same period a year earlier, largely due to the strong sales of its AI chips for use in servers. The majority of Nvidia’s sales now comes from its Data Center business, which saw a 409% increase in revenue for the year. Over half those sales went to the major cloud computing providers.

Nvidia also reported that the shortage of its most powerful chips, the H100, is finally clearing, though it also said it expects to face similar supply constraints when it releases its next generation chip, called the B100, later this year.

The

currency market is a dynamic and ever-changing landscape, and market participants

are always looking for opportunities to profit from the fluctuations of

different currencies. As we navigate through 2023, both the Japanese yen (JPY)

and the Chinese yuan (CNH) are reaching their lowest levels since the global

financial crisis of 2008.

There are a number of factors that suggest that the US dollar could continue to strengthen against the Japanese yen (JPY) and the Chinese yuan (CNY). This could create an opportunity for investors to short these currencies, which means betting that their value will decline.

USD against Japanese Yen weekly Chart USD against Chinese Yuan weekly Chart

The

Robust US Dollar

There are a

number of reasons why the US dollar is expected to remain strong in 2023.

First, the Federal Reserve (Fed) has been raising interest rates in an effort

to combat inflation. This has made US dollar-denominated assets more attractive

to investors, as they offer higher yields. Second, the US economy is still

relatively strong, despite some recent headwinds. This makes the US dollar a

more attractive currency for investors who are looking for a safe haven.

Furthermore, the ongoing conflict in Ukraine fosters an environment of

uncertainty, solidifying the dollar’s position as a dominant player in currency

markets.

The

Weakening Yen and Yuan

Both the

Japanese yen and the Chinese yuan have recently weakened against the US dollar.

Since mid-January this year, the yen and yuan have fallen by about 10% against

the US dollar. Several factors contribute to this weakening, including:

The Bank of

Japan’s (BoJ) continued commitment to loose monetary policy, which has made the

yen less attractive to investors.

The Chinese

government’s efforts to prop up the yuan, which have been met with limited

success.

Concerns

about the economic outlook for both Japan and China.

The

Opportunity to Short the Yen and Yuan

The

combination of a robust US dollar and weakening yen and yuan presents investors

with an opportunity to short these currencies. Shorting a currency entails

betting on its value declining. If the yen or yuan weakens further, investors

who have shorted these currencies could realize substantial profits.

However,

it’s essential to recognize that currency markets are volatile and can rapidly

shift in either direction. Investors considering shorting currencies should

thoroughly understand the associated risks and proceed only if they possess a

strong grasp of currency market dynamics.

Conclusion

In summary,

several factors suggest that the US dollar could continue its strengthening

trend against the yen and yuan in 2023. This potentially creates an opportunity

for investors to short these currencies. However, it’s important to acknowledge

that markets can reverse direction due to various circumstances.

Disclaimer:

The information provided in this article is for informational purposes only and

should not be considered as financial or investment advice.

The Mexican

peso is one of the best-performing currencies in recent years, it has

appreciated more than 10% against the dollar, euro since the beginning of the

year.

Forex – USD/MXN Chart

Introduction:

The Mexican

Peso (MXN), the official currency of Mexico, has gained substantial attention

from traders owing to its remarkable appreciation since April 2020. In this

blog, we will explore the performance of the Mexican Peso, analyze the factors

shaping its value, and uncover the reasons behind its allure for traders

seeking lucrative opportunities in the forex market.

Performance

of the Mexican Peso:

The Mexican

Peso has exhibited resilience and strength in the face of economic challenges,

showcasing impressive performance against other major currencies. Since

reaching a low point in April 2020, the Peso has surged more than 35%,

attracting traders’ interest and positioning itself as a prominent player in the

financial markets.

Factors

Influencing the Mexican Peso:

The robust

performance of the Mexican Peso can be attributed to several key factors:

Strong Economic

Recovery: Mexico’s economy has been witnessing a robust recovery from the

pandemic-induced slowdown. As the nation’s economy gains momentum, investors

are increasingly drawn to the potential for higher returns, thus driving up

demand for the Mexican Peso.

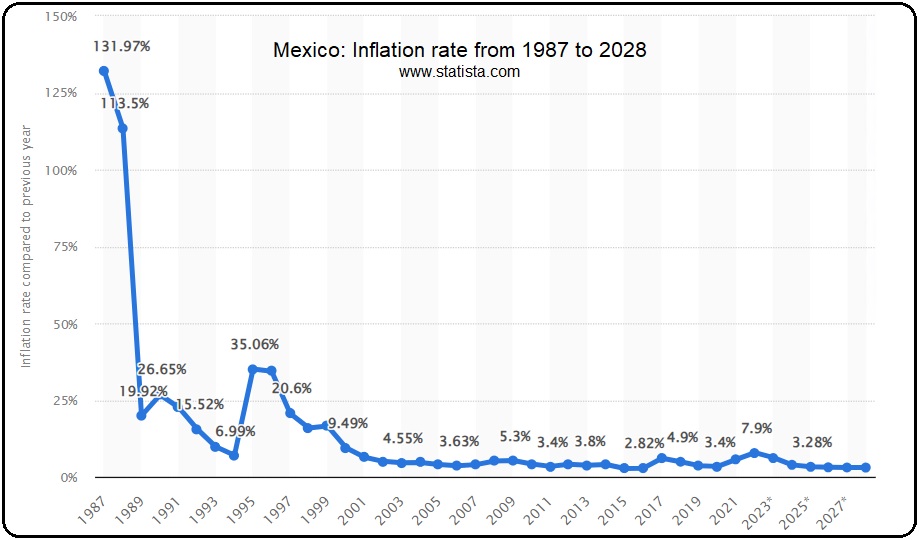

Slowing

Inflation: Mexico’s inflation rate has been on a downward trajectory, creating

a conducive environment for the country’s central bank to implement monetary

policies that support the stability of the Peso. Lower inflation contributes to

a more favorable investment climate.

According to

economists in the most recent Citibanamex survey published last week, inflation

at the end of 2023 is expected to be 4.66%, down from a forecast of 4.99% in

June. The core forecast estimates have also inched down to 5.17% from 5.30%.

Mexico’s inflation has continued its gradual slowdown in early July, aligning

with forecasts, aided by double-digit interest rates and a robust peso.

Mexico Inflation Rate

Improved

Investor Sentiment: Emerging market currencies, including the Mexican Peso,

have gained traction among investors due to improved sentiment. As global

investors seek higher yields and diversification, the Mexican currency emerges

as an attractive option.

Tesla and other

companies plan to open factories in Mexico, taking advantage of the country’s

low labor costs and strategic location, have bolstered investor optimism. The

opening of these factories could have several positive effects on the Mexican

economy, including job creation, increased exports, and improved business

climate. These factors could further strengthen the Mexican Peso.

Outlook and

Trading Opportunities:

The outlook for

the Mexican Peso remains optimistic, with traders closely monitoring the

currency for potential opportunities. The ongoing economic recovery is likely

to fuel the Peso’s upward trajectory, presenting favorable conditions for

profitable trades.

Conclusion:

The Mexican

Peso’s continued strength and positive outlook have captured the attention of

traders worldwide. With a resilient economy, decreasing inflation, and enhanced

investor sentiment, the Peso is well-positioned to sustain its upward

trajectory. Traders looking for promising opportunities in the forex market should

closely monitor the Mexican Peso, as it promises substantial gains amidst its

impressive performance. However, there

is always the risk of political instability. This could weigh on the peso if

it leads to uncertainty about the country’s future.

Disclaimer:

The information provided in this article is for informational purposes only and

should not be considered as financial or investment advice.

Chocolate is set to get more expensive as cocoa prices soar to seven-year highs. Cocoa price has risen by almost 30% in 2023.

Commodity – Cocoa Price Chart 2023

Introduction:

As cocoa prices continue to soar and the industry faces

supply concerns, many are wondering if cocoa is a good investment choice. In

this article, we will examine the factors driving the cocoa market and explore

the potential opportunities for investors.

Record Trading Volume and High Participation:

According to reports, the first half of 2023 witnessed a

record number of cocoa futures and options traded, indicating strong customer

engagement. Cocoa futures hit successive volume and open interest (OI) records,

reaching a record high of 1.4 million contracts on June 29, 2023. Furthermore,

participation in ICE’s New York and London Cocoa contracts is at its highest

since 2018, with record participation in ICE’s London Cocoa markets in June.

Supply Concerns and Demand Increase:

Persistent concerns of low supply from the world’s top cocoa

producers have contributed to the upward momentum of cocoa prices.

Above-average rain in the Ivory Coast and poor weather conditions in Ghana have

flooded plantations and hurt crop prospects, leading to a supply deficit. The

International Cocoa Organization forecasts a global supply deficit of 142,000

tonnes, more than twice the previous estimates. On the demand side, leading

companies like Hershey and Mondelez have experienced a surge in demand,

supported by the reopening of the global economy and growing middle class in

countries like China and Indonesia.

Market Performance and Predictions:

Cocoa prices have reached a 7.5-year high, hovering above

$3,300 per tonne. The price increase has been significant, with cocoa trading

~36% above the lowest level in 2022 and ~93% higher than its 2018 lows. This

surge in prices is attributed to ongoing supply and demand imbalances in the

industry. However, factors such as ageing cocoa farms, climate change, and

long-term buying contracts of major chocolate companies impact the market

dynamics.

Market Analysis and Potential Opportunities:

From a technical perspective, cocoa prices have shown a

strong bullish trend, breaking important resistance points and indicating

potential for further price gains. Traders should be aware of the possibility

of short pullbacks before the continuation of the bullish trend. The market

dynamics make cocoa an attractive option for investors looking to capitalize on

short-term and long-term price movements.

Conclusion:

As cocoa prices reach new highs and supply concerns persist,

investing in cocoa presents an interesting opportunity. Factors such as supply

deficits, increasing demand, and technical indicators support the potential for

further price gains. However, it’s essential for investors to consider the

unique market dynamics and factors that can impact cocoa prices. By staying

informed and understanding the risks and opportunities, investors can make

informed decisions in the cocoa market.

Disclaimer: The information provided in this article is for

informational purposes only and should not be considered as financial or

investment advice.